Gnanasekar Thiagarajan's Blog

Important points for investors to reflect upon before trading Gold

Blogs

Written by GNANASEKAR THIAGARAJAN.

PUBLISHED IN COMMODITIES.

Important points for investors to reflect upon before trading Gold futures and Spot Markets

06 Jan 2020

Important points for investors to reflect upon before trading Gold futures and Spot Markets

Important points for investors to reflect upon before trading Gold futures and Spot Markets

06 JANUARY 2020 | WRITTEN BY GNANASEKAR THIAGARAJAN. PUBLISHED IN COMMODITIES.

Upanishads advise mankind who is seeking happiness to look at oneself and bring about the change rather than trying to change the world and circumstances. Similarly one should understand clearly what kind of investor you are before trying your hand at gold investment/speculation. There are different market participants who use the futures and spot platform as per their needs and objectives. One need to know clearly the kind of investor/speculator you are and accordingly layout some rules and disciplines before trading. There is no point trying to become a long-term investor after the trade goes against you.

Warning: count(): Parameter must be an array or an object that implements Countable in /home/njo3x1tt59uw/public_html/templates/sandal/html/com_k2/templates/default/item.php on line 187

- One needs to do his/her homework on the products available in the exchanges rather than depending on the intermediary to educate them. Intermediaries also do a good job, however the right approach will be to do one’s own homework. All the exchange websites carry humungous amount of information and their staff are quite approachable to for any help. Investors desirous of trading in gold should take this basic effort at least. Once understood, select National Spot exchange if you simply believe in the long-term story of gold or Futures exchanges like MCX which has maximum volumes, if you want to dabble in futures and move with the momentum both ways by trying to profit by buying and selling both or a combination of the above.

- Understanding the dynamics of the gold thoroughly and completely. Instead of blindly believing in views and in greed to make a quick buck, do not jump into the bandwagon blindfolded. Be greedy to acquire more information. Unlike, in the past there is an overkill of information and views on blogs and forums that is likely to confuse you more than providing clarity. However, there are also websites that provide quality views and news that can be used effectively. The key to understanding the dynamics for gold, is to be absolutely clear that gold is not only a commodity which is subject to demand/supply, but it is also a alternative currency, portfolio diversifier and a store of value. Therefore, there are variety of factors that affect and benefit it from time to time. Therefore, it takes a while to put the puzzle together. After having been an analyst, trader and a market participant for 20 years watching gold prices, even today it is foolish to claim to have understood/mastered the dynamics, as new factors appear constantly to influence prices. Once again I am tempted to the Upanishadic wisdom here. “To just go with the flow and reject nothing”!

- Understanding the Risks involved. It is mandatory for all IPO’s to declare the risk factors to investors. Similarly one needs to understand the risks involved, when to stay away from gold. Also, to understand one’s risk appetite before even placing a trade. The most common mistake is to get carried away by market forces when prices are near/at its highs and bottoms due to either greed or fear. This is applicable to other asset classes like equities, where a wrong intra-day trade invariably becomes a long-term investment. This approach will just rattle the investor, specially the one who comes to test waters in gold as an asset-class. A reputed fund manager in Fidelity Investments, Boston, who manage billions of dollars says “ I like to think being wrong in OK, but staying wrong in career ending”. Adhering to stop losses and measuring one’s ability to withstand a certain loss, due to a strong view, hunch has to have a full stop somewhere. With HFT’s and algorithmic trading on the rise, it is absolutely necessary to especially traders in Gold futures to mitigate risk by using stop losses.

- As much as one measures the risks involved, one needs to also be prudent in taking profits from the table when it is there. This approach works well for short-term traders trading gold futures. Even though long-term investors are holding physical/futures positions with a higher target objective, even here it is prudent to offload a portion of the holdings once the returns cross a certain percentage of expectations. Since, gold is traded round the clock and prices are influenced by different factors, a potential overnight profit could turn into a loss. Contentment is the key for market participants in futures. The more contended you are the more chances of ending up the year on a profit. “Be thankful for what you have; you’ll end up having more. If you concentrate on what you don’t have, you will never, ever have enough” ? Oprah Winfrey.

- After all the above is duly considered and acted upon, one needs to get really lucky in getting the right intermediary to assist you to trade/invest in gold. As much as there are professional intermediaries who guide their clients, always putting the clients interest ahead of theirs, there are also many, who induce the clients to trade when one needs to stay away from the market for a personal gain. Therefore, if you are doing your homework well, you don’t need an intermediary to assist you in decision making, but an effective intermediary who can swiftly and efficiently execute trades alone for you.

Therefore, before dabbling in speculation of bullion markets, consider the above pointers carefully and may god bless you all with a good intermediary who puts the client’s interest ahead of his and happy trading!

Written by GNANASEKAR THIAGARAJAN.

PUBLISHED IN COMMODITIES.

The Hedging abuse in commodity markets

10 Dec 2019

The Hedging abuse in commodity markets

The Hedging abuse in commodity markets

The Hedging abuse in commodity markets

10 DECEMBER 2019 | WRITTEN BY GNANASEKAR THIAGARAJAN. PUBLISHED IN COMMODITIES.

The most abused financial instrument called “Hedging” in Commodities

The commodity markets were intended to help agricultural producers manage risk and find buyers for their products. The stock and bond markets were intended to create an incentive for investors to finance companies. Speculation emerged in all of these markets almost immediately, but it was not their primary purpose.

Hedging involves taking an offsetting position in a derivative in order to balance any gains and losses to the underlying asset. Hedging attempts to eliminate the volatility associated with the price of an asset by taking offsetting positions contrary to what the investor currently has.

The main purpose of speculation, on the other hand, is to profit from betting on the direction in which an asset will be moving. Speculators make bets or guesses on where they believe the market is headed. For example, if a speculator believes that a commodity, is overpriced, he or she may short sell the respective commodity futures and wait for the price it to decline, at which point he or she will buy back the stock and receive a profit. Speculators are vulnerable to both the downside and upside of the market; therefore, speculation can be extremely risky.

Overall, hedgers are seen as risk averse and speculators are typically seen as risk lovers. Hedgers try to reduce the risks associated with uncertainty, while speculators bet against the movements of the market to try to profit from fluctuations in the price of commodity futures.

Warning: count(): Parameter must be an array or an object that implements Countable in /home/njo3x1tt59uw/public_html/templates/sandal/html/com_k2/templates/default/item.php on line 187

In most cases, in the name of hedging, speculative bets are taken forgetting the underlying purpose for which the commodity derivatives markets were discovered. The abuse is very profound in agri commodities and to some extent in non-agri commodities as well. In agri-commodities, very few market participants use them as a “perfect hedge”. We have come across many instances where corporations instead of hedging their price risk, tend to increase the price risk further by taking additional speculative bets in futures mostly driven by greed. It does pay off some times, but most of the times leads to huge losses both in the underlying and the futures.

As examples of hedging, consider a food-processing company and the farmer who raises or grows the ingredients the company needs. The company may look to hedge against the risks of price increases of key ingredients — like grains, cooking oil, or soft commodities — by buying futures contracts on those ingredients.

That way, if prices do go up, the company’s profits on the contracts help fund the higher prices it has to pay to make its products. If the prices stay the same or go down, the company loses only the price of the contract, which may be a fair trade-off to the company.

The farmer/grower raising grains, soybeans, or pepper, cotton and coffee, on the other hand, benefits if prices go up and suffers if they go down. To protect against a price decline, the farmer would sell futures on those commodities. His futures position would make money if the price went down, offsetting the decline on his products. And if the prices went up, he’d lose money on the contracts, but that would be offset by his gain on his harvest.

For corporations desirous of offsetting their price risk in commodities, understanding their own organization’s risk appetite is the first and foremost step to arrive at a proper hedging solution and to put in a hedging policy in place. If the risk appetite is less (low risk) and the organization averse to risk, then almost eighty to ninety percent can be hedged leaving scope for just ten percent speculation. In cases where risk appetite is zero (no risk) and the organization just wants to lock the margins and happy as long as there is now downside risk, then a back to back hedge is recommended which is almost hundred percent. In the case of an organization which has some risk (medium risk) appetite at the same time if the underlying quantity has gone beyond the minimum capacity to hold, that much which is beyond the capacity to hold should be hedged. The three categories mentioned above, namely, low risk, no risk and medium risk qualify for the category “hedgers”. Someone with high risk appetite will come under the category called “Speculator” only.

CFTC, the regulator for commodities trading in the U.S, has clearly classified and urges the exchanges to do the necessary homework on what kind of trades take places in commodity futures and what nature they are( speculative or hedge). Such an exercise by the FMC (Forward Market Commission), the domestic regulator for commodities in India, will further strengthen the regulatory mechanism and avoid excessive speculative activity specially in agri commodities, which affect the common man’s interest. Once the FCRA bill is cleared by the Indian parliament, FMC could get more autonomy and resources to implement such globally time tested methods to avoid excessive speculation.

Markets have both hedgers and speculators in them. Knowing that different participants have different profit and loss expectations can help you navigate the turmoil of each day’s trading. And that’s important, because to make money in a zero-sum market, you only make money if someone else loses.

Written by GNANASEKAR THIAGARAJAN.

PUBLISHED IN COMMODITIES.

Manipulation of Commodity Futures Prices-History repeats itself

20 Nov 2019

Manipulation of Commodity Futures Prices-History repeats itself

Manipulation of Commodity Futures Prices-History repeats itself

20 NOVEMBER 2019 | WRITTEN BY GNANASEKAR THIAGARAJAN. PUBLISHED IN COMMODITIES.

Prevention and deterrence of manipulation are major objectives of the regulation of futures market worldwide. Recent instance of manipulation on futures exchanges has sadly seen history repeat itself over and over again and in the very same exchange, which has had a history of similar instances in the past. Surprisingly, not only other agri commodities like Guar seed and Chana, but in the very same commodity, Castor seed few years back in 2016.

This either means that, for reasons best known to the regulators and the exchange involved, a blind eye is being turned towards such manipulation, or the regulator being new to this market is finding it difficult to get a grip of the situation and is being consumed by other issues plaguing the equity markets presently, which takes priority over commodity markets.

There were signs of trouble brewing in castor seed futures, which NCDEX should have ideally spotted early with better monitoring. Alarm bells started ringing for NCDEX after officials realised that a large section of buyers was excessively leveraged and might not have over 5 bln rupees needed to honour the delivery. The way in which NCDEX and its clearing corp handled this castor seed crisis threatens to create a major trust deficit among participants in the commodity market. However, this column is not to add oil to fire, but to suggest a possible permanent solution, so that such instances does not recur again, and more so in Agri commodities. And in that specifically in commodities without an international reference or benchmark.

Warning: count(): Parameter must be an array or an object that implements Countable in /home/njo3x1tt59uw/public_html/templates/sandal/html/com_k2/templates/default/item.php on line 187

A POSSIBLE AND CREDIBLE SOLUTION

Though this has been suggested by experts in the past, due to the current circumstances, it is hugely relevant and only re-affirms and revives that suggestion to be taken seriously by the regulators and policy makers.

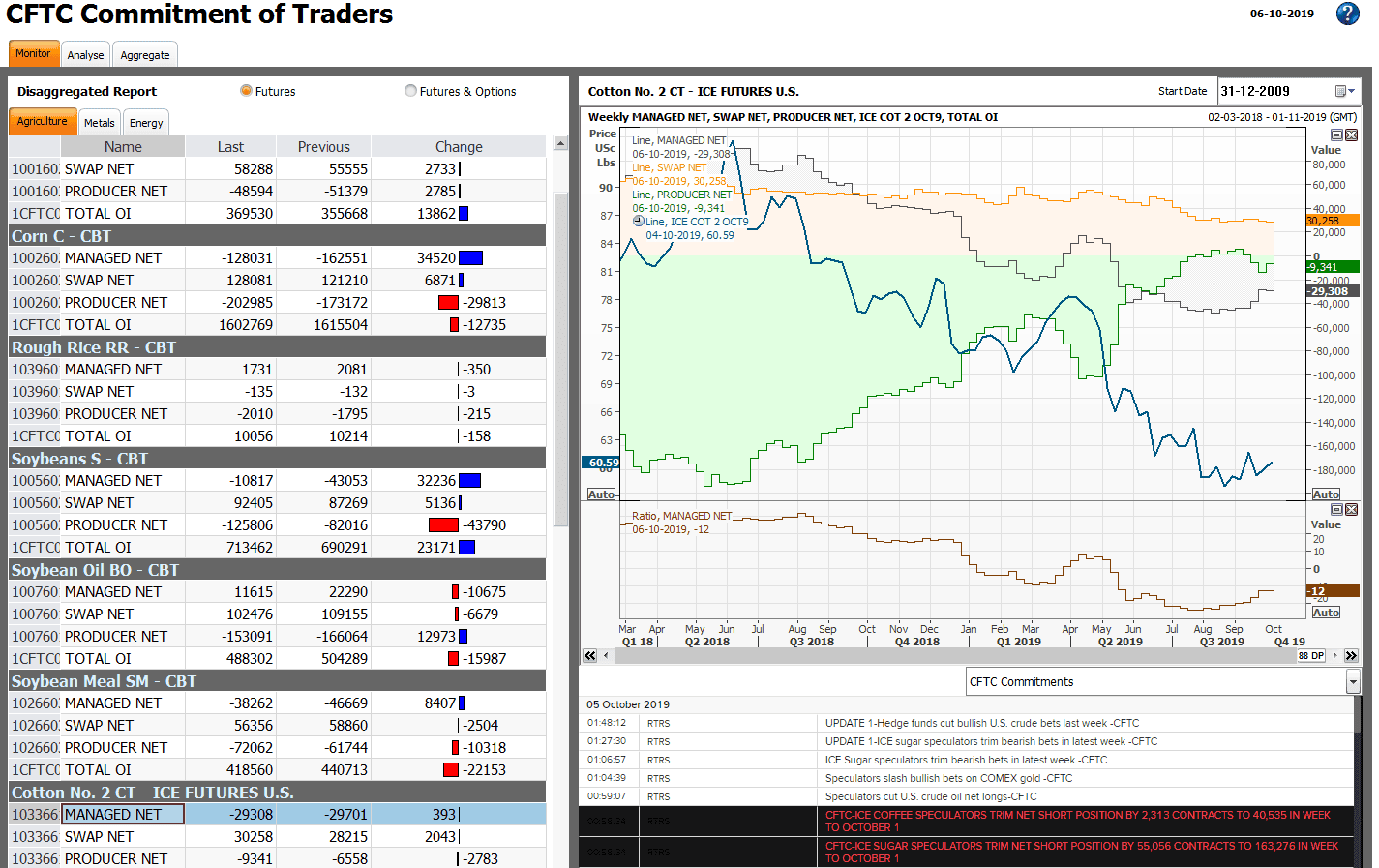

Apart from few instances of manipulation in commodity futures in the US, it has never come to an extent of banning a contract, or a settlement crisis, thanks to the robust mechanism that catches any aberrations in the futures prices and sends alarm bells ringing way ahead. We are not talking about any sophisticated risk management procedures here, but a wonderful and transparent compulsory reporting called, The Commitments of Traders report ( COT), that is published every week that even helps investors predict the price movement, over and above being an early warning system for the regulator and exchanges.

The Commitments of Traders is a weekly market report issued by the Commodity Futures Trading Commission (CFTC) enumerating the holdings of participants in various futures markets in the United States. It is collated by the CFTC from submissions from traders in the market and covers positions in futures on grains, cattle, financial instruments, metals, petroleum and other commodities. The Commodity Futures Trading Commission (CFTC) releases a new report every Friday at 3:30 p.m. Eastern Time, and the report reflects the commitments of traders on the prior Tuesday. The weekly Commitments of Traders report is sometimes abbreviated as "CoT" or "COT."

The report was first published in June 1962, but versions of the report can be traced back to as early as 1924 when the U.S. Department of Agriculture’s Grain Futures Administration started regularly publishing a Commitments of Traders report.

The report provides a breakdown of aggregate positions held by three different types of traders: “commercial traders,” “non-commercial traders” and “non-reportable.” “Commercial traders” are sometimes called “hedgers”, “non-commercial traders” are sometimes known as “large speculators,” and the “non-reportable” group is sometimes called “small speculators.”

The CoT report is keenly awaited by traders to gauge the trend in the market by analysing the changes in the positions of large speculators and/or commercial traders (hedgers). Many traders use the CoT report to bet in the direction of non-commercial traders, as it found in the last many years that this category of traders is usually on the right side of market. Some track non-reportable (small speculators) positions, as they believe that this category of traders is on the wrong side of the price direction.

Source: CFTC , Reuters

An example of the weekly CFTC report on cotton , can be seen above.

I strongly believe that this mechanism of voluntary disclosure by market participants could be an ideal solution. If the biggest commodity futures markets in the US, are relying on it and there has not been any major instances of manipulation, why can't we take inspiration from it, than constantly rubbishing it as too early for the Indian market system to implement? Many in the exchanges and the policy makers believe that Indian commodity derivatives markets are still not mature enough to have a CoT-like system. It has been almost 15 years since commodity futures were nationalized, and it is sad that we have not even taken baby steps to implement such a system. This could bring in greater transparency in policy formulations and also to set limits for different trading categories and avoid such repeated instances of failures that dampen sentiment for commodity markets in India as a whole.

CONCLUSION: Assuming the system was in place, both the regulators and the exchange would have been quick to spot the balooning open interest, which was almost a quarter of total production. When the Non Commercial positions ( Large speculators) positions increased/decreased on a weekly basis, both would have been quick to act by increasing margins, or the circuit filters, or dealing with it appropriately in any other way.

Written by GNANASEKAR THIAGARAJAN.

PUBLISHED IN COMMODITIES.

Importance of emotional stability for trading in edible oil futures

19 Nov 2019

Importance of emotional stability for trading in edible oil futures

Importance of emotional stability for trading in edible oil futures

19 NOVEMBER 2019 | WRITTEN BY GNANASEKAR THIAGARAJAN. PUBLISHED IN COMMODITIES.

Emotional stability is so very important when it comes to futures and options trading , or derivatives trading. In my twenty years experience in dealing with commodity futures, I have seen many corporations and individual traders in the edible oi industry who are tigers on physical trading, but pussy cats when it comes to futures trading.

They are not afraid to run huge losses in the cash market hoping for prices to move in their favour, but that is not the case when it comes to futures trading. The same tigers are so impatient when it comes to their stop loss getting hit in futures. They get so irritated and loose their mental stability, which is so pertinent in commodity futures trading.

The most important risk management strategy in futures trading is a stop loss. I have tried so many many times to drill this concept of stop loss into the minds of traders and needless to say only a handful have understood and embraced the concept so far. I think it is mostly due to their confidence in holding on to cash market positions that bleed out of the money only to come back in money subsequently. But, this holding period comes with huge amount of stress, hope and loss of health. Suddenly, god comes into the picture and deals are done with Lord Balaji the deity for prosperity to rescue out of the situation. After the cash position comes back in the money, a visit to Tirupathi is a must to thank god for his kindness and pay back the promised debt.

Warning: count(): Parameter must be an array or an object that implements Countable in /home/njo3x1tt59uw/public_html/templates/sandal/html/com_k2/templates/default/item.php on line 187

Unfortunately, none of this is possible in futures trading. Even god can’t save you, if you do not adhere to a stop loss. In cash markets, one holds on to a position hoping it will come back in favour , if the same strategy is adopted in derivatives too (Goom phirke wapas ayega), a very costly and dreadful experience will be in the offing. As the positions goes out of money, the intermediary will be breathing down the neck for mark to market margins and a cash flow implication for the accounts department to deal with reluctantly. So, stop loss is so sacrosanct for futures trading. And for that knowledge of technical analysis and other price studies will help a lot, rather than relying on vomited information( S&D’s) that is already known to the market. With all due respect, funda-mentals are needed, but one needs to know when not to use them, especially in an over-heated market condition like the CPO futures markets witnessed in the past few weeks. The inability to give back some money to the market by way of a stop loss, is the foundation for a huge loss staring at one’s face in the future. So, emotional stability comes, when one knows that stop losses might get triggered, but they protect as an insurance against price risk and therefore, not get carried away by market moves and stick to the trading plan as long as the stops are in place.

CPO prices shot up in BMD on the back changing fundamental picture overseas and in reaction to that domestic prices were on a roll in India and MCX prices reached a boiling point. From the time prices crossed 620 in MCX, it has been super overbought, a technical term used by chartists and price hunters, which obviously is not agreed by the industry and fundamental followers, as there has been a flurry of news flows re-affirming more upside. The important and basic principle of price studies and analysis is that all fundamental factors are already factored into the price and price itself is a lead indicator for direction.

We had recommended and initiated trading positions on the sell side as per technical analysis. It is like going counter to the trend. But with a stop loss, counter trend works well, because the risk is limited and one can take advantage of the subsequent downside correction. Time and Price have a close relationship like a husband and wife, but when price seeks happiness elsewhere and runs away, it only lasts for some time. Price is the husband and the wife is time. When price overshoots time, meaning if prices run away in a short period of time, it might not last long, because it has to come back into the relationship with time sooner or later. Which is what is also signified as overbought in technical parlance. Any sharp move in prices will exhaust itself sooner or later, like a trekker who reached the peak and no more upside to go, but only downside.

No one can predict a top, which is why there is a plan ‘B’ called stop loss. In case, you get it wrong you loose a tiny bit, which can be easily recovered over time. However, if you don’t adhere to a stop , then it could be very costly and the recovery will become the goal rather than making new profits. The industry was mostly on the buying side waiting for a correction, which was elusive and that added to stress levels for holders of short positions. Even though BMD futures corrected almost 100 points from their peak as expected, domestic prices were unmoved largely due to a weakening local currency and an expected rise in tariffs by the Customs.

As is always the case, it was a buy on rumor and sell on news that unfolded. Post the news, prices tanked lower. These patterns of market behaviour is captured in the price, which is then visible in a chart for the technical analyst to predict future price movement. Patterns are formed from habits by market participants and similar reactions to situations in the past. It is not easy to be sitting in a counter trend position and during the process an emotionally stable mind is a must, not to get carried away by market forces. A successful trader is the one who sees opportunity during adversity and vice versa. Most mistakes are committed either due to greed or fear. These are the two forces always in play in the minds of a trader that influences his/her trading decisions.

Only an emotionally stable person can reach greater heights in trading by moving with the flow of the markets and maintaining an equipoise, neither elated during success, nor dejected by failure.